By: Prof. Dr. Fazal Rehman | Last updated: February 3, 2024

[OBJECTIVE]Subject: Applied Econometrics (Theory)

Time Allowed: 15 Min

Total Marks: 10

NOTE:ATTEMPT THIS PAPER ON THIS QUESTION SHEET ONLY. Division of marks is given in front of each question. This Paper will be collected back after expiry of time limit mentioned above.Part-I State whether the statement is true or false, each question carries equal marks. (10)

The method of OLS is not applicable to estimate a structural equation in a simultaneous-equations model.

Two stage least squares method is applicable for under identified equation.

In the presence of a stochastic regressor(s) and an autocorrelated error term, the method of instrumental variables will produce unbiased as well as consistent estimates.

Underfitting a model (omitting relevant variable(s), L.S. estimators are biased as well as inconsistent.

The D.W. d test assumes that the variance of the error term is homoscedastic.

If heteroskedasticity is present, the conventional t and F test are valid.

Despite perfect multicollinearity, OLS estimators are BLUE.

For quarterly data, we should define three dummy variables to check seasonality of the data.

In Aitken Theorem, error terms of GLR model are Non Spherical.

Even though the disturbance term in the classical linear regression model is not normally distributed, the OLS estimators are still unbiased.

[SUBJECTIVE]Subject: Applied Econometrics (Theory)

Time Allowed: 2 Hour 45 Min

Total Marks: 50

NOTE:ATTEMPT THIS (SUBJECTIVE) ON THE SEPARATE ANSWER SHEET PROVIDEDPart-II Give short answers, each question carries equal marks. (20)Q#1: Assumptions of generalized least squares

Q#2: Heteroskedasticity

Q#3: Instrumental variable

Q#4: Indirect Least squares method

Q#5: Geary test for Autocorrelation

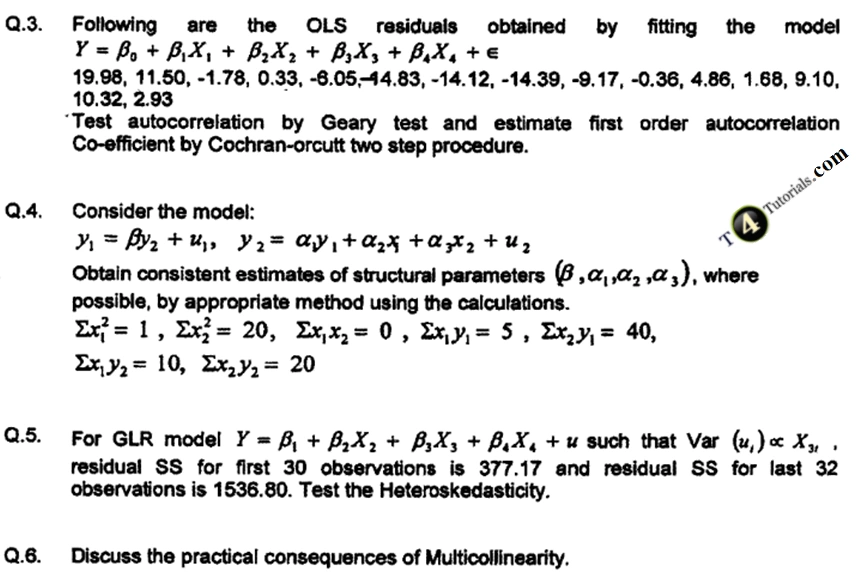

Part-III Give detailed answers, each question carries equal marks. (30)Applied Econometrics Past Papers